Hong Kong stocks too cheap to ignore (part 3)

Dah Sing Banking Group

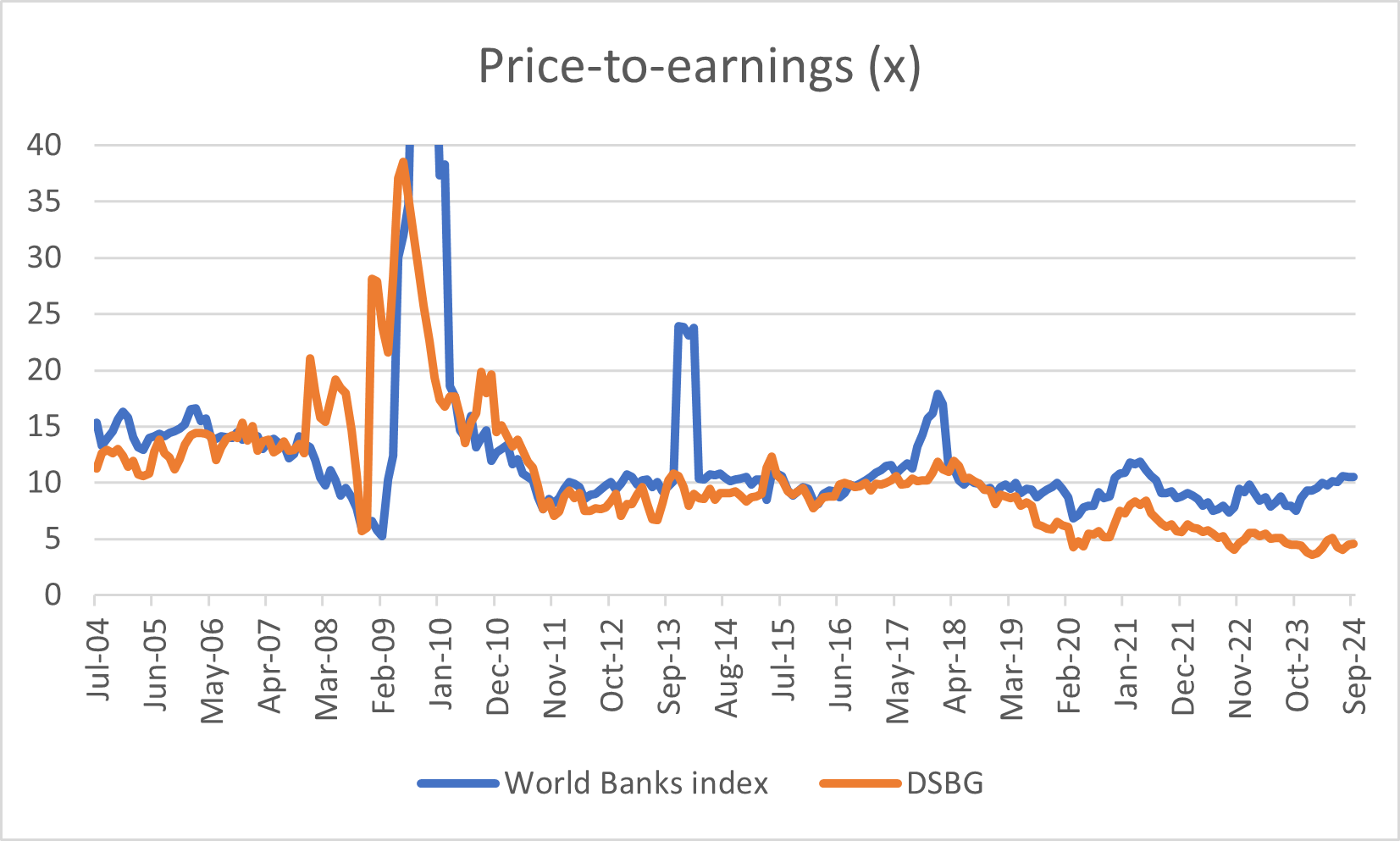

With Hong Kong shares finally receiving some love (benchmark index +39% from the mid-January low) this may be the finale of the ‘Hong Kong stocks too cheap to ignore’ series. With that introduction, let’s look at Dah Sing Banking Group, a small yet solid lender which continues to trade on exceptionally low multiples (0.3x P/TB, 5x P/E, 11% dividend yield) despite a pop from the bottom. Its fair value may be HKD 17 per share, ~140% above the current price. The bank has a strong funding and capital position and is well-regulated. Low multiples protect the shares from downside risk – a perfect asymmetrical opportunity.

Ticker: Hong Kong 2356

Price: HKD 7.04

Mkt Cap: USD 1.3 b

History

Dah Sing Bank (DSB) was founded in Hong Kong in 1947. Its parent company, Dah Sing Financial (DSF), was listed on the local bourse in 1990.

In 2004 DSF created an intermediate holding company, Dah Sing Banking Group (DSBG), to hold DSB and some smaller entities. DSBG went public soon after, with DSF retaining a 77% stake with public investors holding 23%.

The reorganization followed the Closer Economic Partnership Arrangement (CEPA) between Hong Kong and China. CEPA allowed Hong Kong banks to have preferential access to the Chinese banking market, which was still largely closed to foreign lenders.

DSBG began rolling out branches on the mainland. It also acquired a Hong Kong-based non-bank lender and a bank in Macau in 2005. In 2007 it purchased 17% of Bank of Chongqing, a regional bank in China.

Overall, the period ahead of the Lehman bankruptcy was favorable for banks in most geographies. Regulation and capital requirements were light. Economic growth was robust. Deflation and zero interest rates – destroyers of bank loan-deposit spreads - were Japanese oddities.

DSBG earnings dipped in 2008 and 2009, largely due to write-downs of USD structured investments and higher loan losses. From 2010 earnings recovered and peaked in 2018. Since 2019 times have been tougher, first due to political unrest and then due to the pandemic and Hong Kong’s insane public health policies.

Operations

DSB offers a standard suite of banking products and services. Households and SMEs are the key customer segment.

The segment mix of net revenue is 49% Personal Banking, 21% Corporate Banking, 20% Treasury & Global Markets, and 10% Mainland China and Macau.

The revenue mix is normal for a bank – in 1H 2024 net interest income was 77%, net fees 18%, and trading/other 5%.

Business Quality

DSBG has reported 9% average ROE since 2004. There have been two strong periods (2004-2006 and 2013-2015) and some leaner times (2008-2009, 2020-2023). To put this into perspective, HSBC hasn’t done any better (also 9%) and JP Morgan only modestly so at 11%.

For years the Hong Kong banking industry has been dominated by HSBC and its 64%-owned Hang Seng Bank, along with Bank of China (Hong Kong) and Standard Chartered. Combined, these four players control ~65-70% of the market. There are ~25 other fully licensed banks, including DSB and 8 ‘virtual banks’ which received licenses a few years ago. DSB’s market share is ~1%.

The big players could probably price DSB and the smaller banks out of business. But they don’t. Regulators want stability, not price wars and bank runs.

Virtual banks’ entry has surely been the biggest competitive threat to Hong Kong’s incumbent lenders for some time. How has it gone for the digital banks? Well, they are yet to prove themselves. All are loss-making and a couple a balance sheet contraction in 2023. Presumably the 8 will merge into 2-3 or perhaps be swallowed by incumbent banks. The truth is these virtual banks don’t offer anything unique. Incumbent banks of course offer digital service and can potentially outspend digital banks on IT.

So, Dah Sing is a small player in a market which has grown more competitive. Yet the business has attributes. First is the license itself. The Hong Kong Monetary Authority isn’t keen on issuing lots of new licenses. Second, many banking products (residential mortgages, checking accounts, small business lines of credit) create long-term customer loyalty. These sticky relationships are the dream of all businesses. Third, Hong Kong’s wealthy population affords banks ample opportunities to sell investment and insurance products. This offsets the commoditized nature of loans and deposits.

Cyclical trends

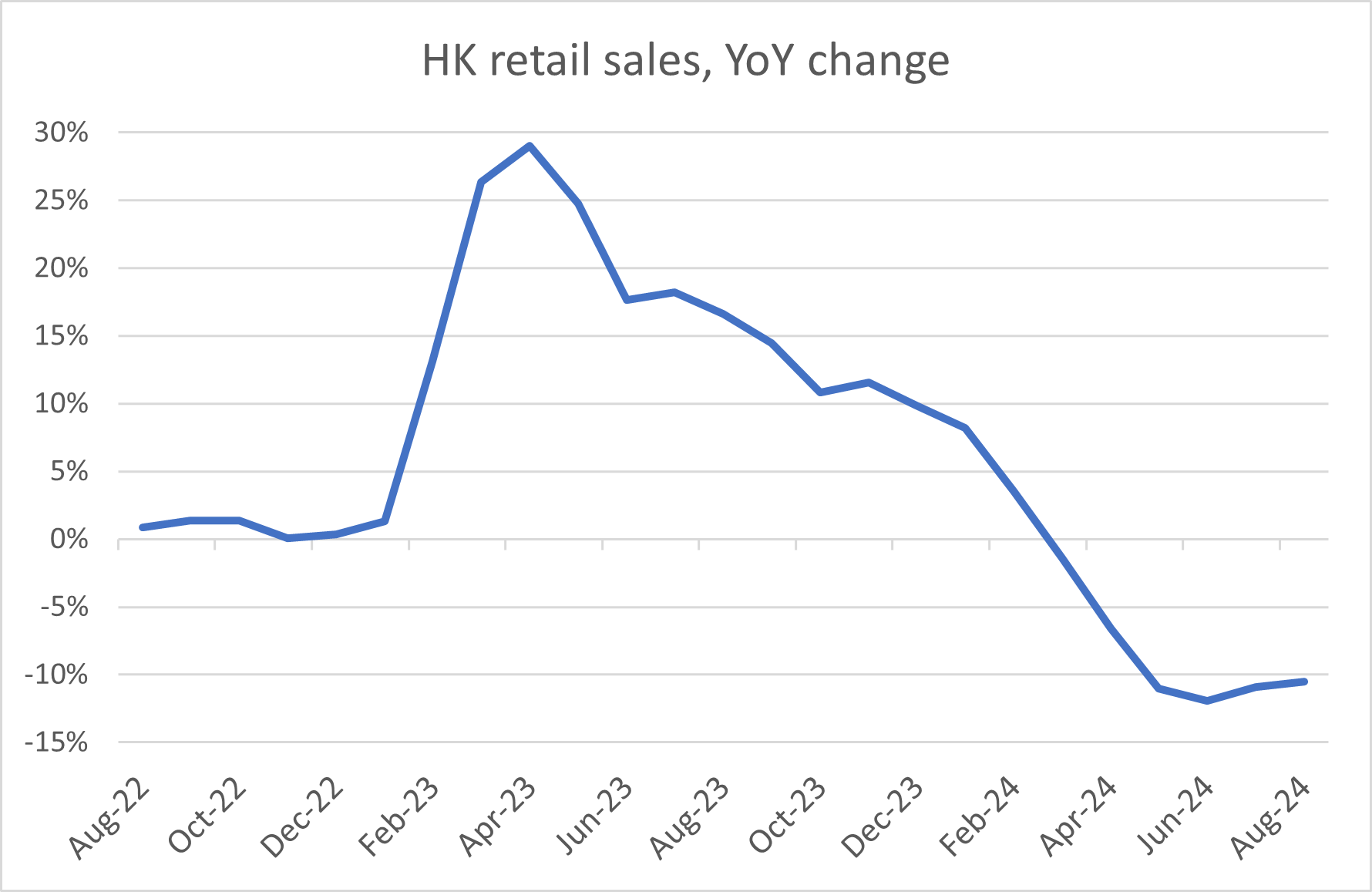

Hong Kong has lost its economic mojo. While inflation and unemployment are low, consumption and the property market remain weak. The revenge spending of mid-2023, as HK/China resumed normality post-pandemic, is now but a distant memory. Residential property prices in August reached the lowest level in 8 years and have declined 27% in 3 years.

Despite the difficult macro environment, DSBG posted healthy figures in June:

· Revenue growth of 22%. Higher interest rates have allowed net interest margin to expand and the strategic alliance with Canada’s Sun Life, which began last year, resulted in more insurance distribution income.

· Good expense controls allowed for the cost-income ratio to decline to 49% from 57% in 1H23.

· The impairment charge for its associate (Bank of Chongqing) fell sharply.

· A higher loan impairment cost was the main negative. This noted, the underlying trends in the loan book showed only modest deterioration.

The US interest rate easing cycle is one reason to be optimistic. The HKD is pegged to the USD and has been for >40 years. This leads to a stable FX rate. It also ties Hong Kong interest rates to the US, which can be inappropriate at times. Like in 2022-2023, when, through the peg, Hong Kong was effectively tightening monetary policy into a weak economy. Ouch.

Thus, the recent 50 bps reduction in the Fed Funds rate was met with a 50-bps reduction in the Hong Kong Base Rate and leading banks lowering their Prime Rate (but by just 25 bps!). Further US rate cuts have the potential to lower borrowing costs in Hong Kong, which will be positive for local property prices and therefore consumer confidence and spending.

Balance sheet health

There are three main criteria for measuring balance sheet health of a bank.

· Capital adequacy. More capital implies a more resilient balance sheet, but too much suppresses ROE. DSB is in the later camp. Its Common Equity Tier 1 ratio stood at 16.7% as of June, high by banking norms. (For the world’s largest banks, the average ratio is about 13%). Unlike most large banks, DSB calculates its risk weighted assets (the denominator in the ratio) using the ‘standardized’ method. Most large banks use internal models, which typically allow for a higher capital ratio. Perhaps the best ‘reality check’ on the quality of the calculation is look at RWA density (risk-weighted assets as a % of total assets). For DSB, this figure is 67%. For the world’s largest banks, RWA density is ~40%. Effectively, DSB has a higher capital position based on a more conservative calculation. Over time, DSB may be able to move to an advanced calculation, which could allow it to hold less capital, thereby increasing ROE.

· Funding & liquidity. The loan-deposit ratio is 71%. It has some small balances of interbank funding and long-term debt. It has not taken on excessive duration risk in its bond portfolio (unlike some US banks). A rough estimate is that the duration is 3 years or less. Overall, this is a low-risk funding and liquidity profile.

· Loan quality. Directionally loan quality has softened. This is to be expected in an economy with sluggish growth and deflating property prices. But the numbers are far from concerning. Impaired loans are 2.0% (from 1.9% in December). Allowances and collateral equal 80% of impaired loans. The bank had no material exposure to the large mainland property developers which defaulted in recent years. It is true that cases of negative home equity amongst residential borrowers have increased. But as seen in previous cycles, this doesn’t drive defaults in Hong Kong. In the early 2000s, after a ~65% decline in property prices, the delinquency rate on residential mortgages was <2%.

Management & corporate governance

DSF owns 74% of DSBG. In turn, the Wong family owns 43% of DSF. At the head is the 83-year-old Chairman David Wong. The board is unlikely to challenge him too much, with three executive directors and an ‘independent’ octogenarian director who has served since 2004. The five other directors appear genuinely independent and have credible backgrounds. Waiting in the wings is the Chairman’s son, aged 54, who is the CEO of DSB. Seems odd that he doesn’t sit on the main board.

Overall, public shareholders have been treated fairly by the Wong family. Since the 2004 listing, the average dividend payout ratio has been 35%. Capital allocation has been sensible. With hindsight perhaps the investment in Bank of Chongqing can be questioned, though ‘everyone was doing it’.

Valuation

Banks in most markets have traded on lower multiples in recent years compared to the era before the Lehman bankruptcy. The main issue is structurally lower ROE. On average, ROE for banks globally was 15% from 2003 to 2007 but just 10% from 2010 to 2023. There have been two major drivers:

· Basel 3 increased capital and liquidity requirements.

· Negative/zero interest rates brought bank loan-deposit spreads to low levels.

This second driver, negative/zero interest rates, is no longer relevant. This suggests ROE can improve from 10%, though will probably not reach the 15% of the previous era.

Bank stock multiples in most markets have re-rated. But not DSBG. The stock continues to be weighed down by concerns about whether it and its Hong Kong/China peers are ‘uninvestable’ or not.

From the current 0.3x P/TB and 5x P/E, a re-rating to 0.9x P/TB and 8x P/E (median multiples since 2011) suggests a share price of HKD 17 is achievable. This would be 140% upside from the current HKD 7.0.

Disclaimer: The information contained in this report is for general informational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities or other financial products. The opinions expressed in this report are those of the publisher and are subject to change without notice. Readers are advised to conduct their own research. The publisher does not guarantee the accuracy, completeness, or reliability of any information in this report, and disclaims any liability for any losses or damages arising from the contents of this report. The publisher of the report often invests in companies about which it writes.

I've only come across the holdings company - DSFH... I linked to your post for today's weekly round up: Emerging Market Links + The Week Ahead (October 14, 2024) https://emergingmarketskeptic.substack.com/p/emerging-markets-week-october-14-2024

For US residents, Interactive Brokers allows customers to buy stocks in HK and many other int'l markets. Probably others do as well.