Alico Inc (ALCO)

Liquidation value may be $60, double the current share price

Alico, with 71,803 acres of land carried on its balance sheet at a discount to estimated fair value, is a not unknown asset play. However, the stock hasn’t performed, presumably due to continued disappointment from the citrus farming business and the slow pace of land disposals. Patient investors are likely to be rewarded. Liquidation value may be $60 per share, double the current stock price.

History

In 1960 Atlantic Coast Line Railroad spun-off its landholdings through Alico. In the 1970s, a ‘citrus tycoon’ named Ben Hill Griffin Jr, acquired control of Alico and inserted himself as Chairman. Upon his death in 1990, control passed to his son, Ben Hill Griffin III, who owned ~50% of shares. A family squabble followed. BHG III relinquished his shares to a trust controlled by his 4 sisters. One of their husbands took the CEO job.

In 2013 the finance bros took over. Paying $37 per share, an investor group acquired the family’s ~50% stake and inserted new management. At the time, in terms of land usage, Alico was 52% ranch & conservation, 34% improved farmland (primarily sugarcane production), 13% citrus, and 1% other.

New management didn’t waste too much time in reshaping Alico. It effectively exited the sugarcane business by leasing the acreage to its customer, a sugar processor, in May 2014. In August that year it announced an agreement to sell ~31k acres of sugarcane production land for $98 m. In December 2014 it announced 3 acquisitions of citrus growers for a total consideration of $363 m (~$13,000 per acre). The acquisition positioned Alico as one of the largest citrus growers in the US.

Hurricane Irma, which hit Florida in September 2017, caused significant damage to crop production. Alico received compensation from its insurance policies and federal relief funds.

In November 2017 it announced a new strategic plan. Management made some bold promises about cost reductions, asset sales, and exit from cattle production, and intention to plant more trees to increase citrus production.

In June 2022 it lost a source of revenue when 3rd party grove owners exited the citrus business.

Hurricane Ian, which made landfall in September 2022, was another blow to Alico.

Operations

Alico owns ~72,000 acres of land in 7 Florida counties – Desoto, Polk, Collier, Hendry, Charlotte, Highlands, and Hardee. The land is in central southern Florida, wedged between Tampa and Fort Myers.

The company’s two operating segments follow the management of land holdings:

· Citrus – these operations are on ~49,000 acres of land. The bulk of citrus output is sold to Tropicana and ends up in not-from-concentrate orange juice. Fresh fruit sales are the remaining amount.

· Land Management & Other Operations – span ~23,000 acres of land. Some of the land is leased for recreation, grazing, and mining. Some land is held for conservation. The company opportunistically disposes of acreage.

It also has mineral rights to 90,000 acres.

Business quality

There is much not to like about Alico’s Citrus business:

· Lack of barriers to entry.

· Commodity product.

· Falling demand. Americans consume ~40% less orange juice than they did 15 years ago. This may be to concerns about the sugar content in the juice. Fresh fruit consumption has declined as well, but to a lesser degree, though this is a small % of Alico’s business.

· Output can be negatively impacted by severe weather, disease, and pests. This has been the biggest problem in recent years. Output, in terms of 90 lbs boxes of fruit, peaked in 09/2015 at 10.5 million. Following a sharp decline caused by Hurricane Irma, which hit Florida in September 2017, Alico was optimistic it could return to 10 m boxes output. It hasn’t come close. The twin diseases of citrus greening and citrus canker have weakened output. Hurricane Ian hit. In 10/2023 output was just 2.7 m boxes.

· Capital intensity is high. Growing oranges is not as simple as planting a tree and letting nature work its magic. 25-year useful lives for citrus trees means 4% of the grove must be re-planted annually. It isn’t just the cost of trees – land must be improved, irrigation systems built, and standard farming equipment purchased. For Alico, a capex-sales ratio of 20% is normal. In the last decade, capex has been ~1.8x greater than operating profit.

· The majority of revenues stem from a single customer. Specifically, Tropicana is ~90% of revenue. Good luck bossing them around. Multi-year contracts are set to expire in 2024 and 2025.

The result is an average ROIC of 2% in the past decade. Were land carried at estimated fair value, ROIC would be even less.

If one were looking for positive comments to make, there are some.

· It has scale. In recent years it has produced ~10-15% of Florida’s orange crop. Presumably this means its per unit production costs are lower than competitors, though there isn’t much transparency on this issue.

· Competitors are exiting the market. Currently there are ~2,000 orange growers in Florida compared to ~8,000 several years ago.

· It has water permits in place for the next 15-20 years.

Recent developments & outlook

Results for 09/2023 were weak. Alico was barely profitable due to a poor harvest (damage from Hurricane Ian + ongoing issues with tree disease) and a smaller gain on land disposal.

This sets the stage for a likely higher profit from citrus operations in 09/2024:

· Recovery from Hurricane Ian plus maturation of trees planted in recent years should lead to better harvest.

· From January 2023 it began a citrus greening therapy which could limit the damage caused by disease.

· Potential receipt of federal funds as compensation for Hurricane Ian damage. To put this in perspective, it received $27 m in federal relief funds relating to Hurricane Irma.

In terms of land disposals:

· The sale of 17,229 acres to the state of Florida for $78 m is expected to close in the 1H of the current fiscal year.

· It will commence a multi-year entitlement process on 4,500 acres near Fort Myers, which could result in a transaction at some point.

Balance sheet health

Net debt, at 52% of shareholders’ equity, is not excessive. The bulk of debt does not mature until after September 2028.

Capital allocation

The company’s mantra is to utilize its land holdings to generate the highest return. In the current conditions, it is doubtful that farming oranges is the best use of the land.

Management has stated an intention to use the $78 m of proceeds from the upcoming land sale to repay variable rate debt, which is $45 m. That would leave $33 m remaining. Is there potential for a special dividend or buy-back with the remaining amount?

Management & corporate governance

The 2014 investor group which took control of Alico continues to weigh heavily on the shareholder list. The controlling LLC dissolved in 2019 and distributed Alico shares to its members. 6 individuals may have a combined ~33% of shares.

That group also continues to be represented on the board, holding 4 of 8 seats, including the Chairman role. 3 of the other 4 directors are non-executive and joined between 2019-2020. The CEO rounds out the board.

The CEO has been in the job since July 2019. Prior to assuming the top job he was CFO.

Red flags exist. First, in the 10/2022 there was an admission that internal controls were inadequate and previous figures had to be restated. Miraculously, the result was a $2.5 m increase in net worth (and offsetting reduction in deferred tax liabilities), though hardly something to inspire confidence. Second, there has been turnover in the CFO position. The current CFO started in August of this year. His predecessor lasted less than a year.

The CEO earned $1.3 million in FY 10/22.

Valuation

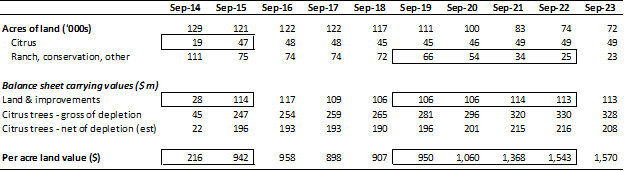

The 71,803 acres of land is an asset that is undervalued on the balance sheet. Including land improvements, as of 09/2023 the per acre carrying value was $1,570, for a total value of $113 m. Not all of this land was purchased decades ago. In value terms, most of it relates to the 2014 acquisition of citrus groves. Land classified as ranch is carried at a much lower per acre value than land classified as citrus, as it was not recently acquired.

The flip side to hidden value in land, however, is the valuation of citrus trees. The gross value is $328 m and, net of depletion, the figure is ~$208 m. Anyone looking to buy Alico’s land to build houses, golf resorts, strip malls, etc, will assign zero value to the trees.

There are other considerations – primarily the purchaser’s use of the land. To date, much of the land has been sold for use in conservation, including the Florida Forever program run by the state. A buyer of conservation land will pay less than a buyer looking to use the land for commercial purposes.

So how to measure the fair value of Alico’s assets?

(1) Land transactions in relevant Florida counties

Zillow data, for land sales in the past several weeks in Florida counties in which Alico has holdings, shows an average per acre price of $16,479. Presumably this land will be used for commercial purposes. Simply applying this per acre price to Alico’s land yields a valuation of $1.2 b. This should be considered an unrealistic ‘best case scenario’. In practice, a portion of Alico land may end up being sold at this price, but certainly not all of it.

(2) Alico realized and contracted disposals

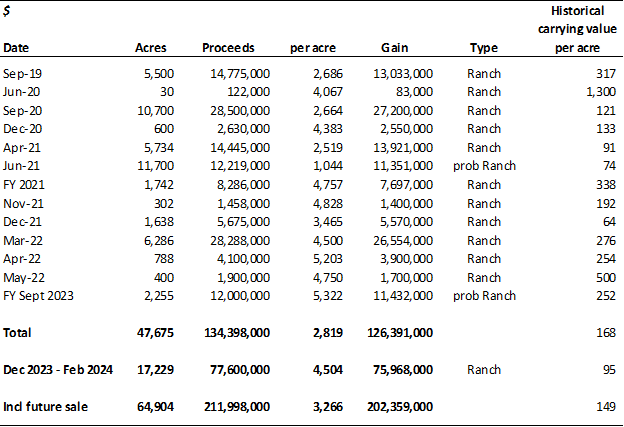

In the past 5 years, Alico has made numerous land sales. Virtually all, if not all, have been land classified ‘ranch’ rather than ‘citrus farming’. This is an important distinction, as there are no citrus trees sitting on ranch land which would potentially have to be impaired. The average disposal was $2,819 per acre. Including the planned sale of 17,229 acres in the 1H of the current FY, the average per-acre proceeds increase to $3,266.

(3) Alico IR material

Alico IR material presents management opinion that the land is undervalued by $505-628 m in total. It is unclear how Alico treats the valuation of trees in this – does management include the value of trees in these figures or ignores a potential impairment?

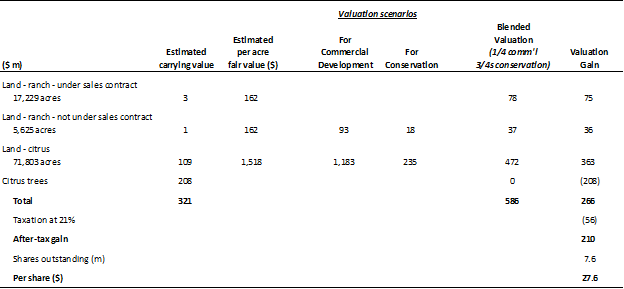

Bringing all this together, what is a reasonable value for these assets? The key assumptions are that ¼ of sales are at commercial prices (i.e., $16,479 per acre), ¾ are for conservation ($3,266/acre), and that the citrus tress are worthless. In summary:

· Ranch land under contract to sell. This is an easy one. The proceeds will be $78 m as announced.

· Other ranch land – estimated value of $37 m.

· Citrus land – estimated value is $472 m.

· Citrus trees. The estimated carrying value is $208 m. Assume a full write-off, as the land would either revert to conservation purposes or be used for development.

In sum, this $266 m gain pre-tax, or $210 m post-tax, which is $27.6 / share. Add this to the reported tangible book of $31.9 per share, and the liquidation value becomes $59.5.